The Debt Ceiling mess will not change our investment strategy

Should we be worried about a default by the US government? We don’t think so and the chart below is the reason why.

Above is the yield on 10 year US Treasury Bonds since the beginning of the year. Now before you nod off at the mention of bonds, let us explain. Since January the interest rate on the 10 year bond has fallen from 3.5% to below 3%—2.91% to be exact. In other words, investors around the world are willing to loan the US government money today at a lower price than they were demanding six months ago. And yet, there’s more talk now of default than at any time since the Civil War.

If the US government was really in danger of default the interest rate on these bonds would be north of 10%.

So the Treasury market is telling us that the default story is phony, but of course that doesn’t mean there’s absolutely nothing to worry about—there’s still Greece. However, the debt ceiling crisis is actually a political crisis having very little to do with a short-term financial catastrophe.

In fact, there’s some reason to hope that the worst of our debt mess is behind us. Debt at corporations is at an all time low and high cash balances are becoming an embarrassment for some companies.

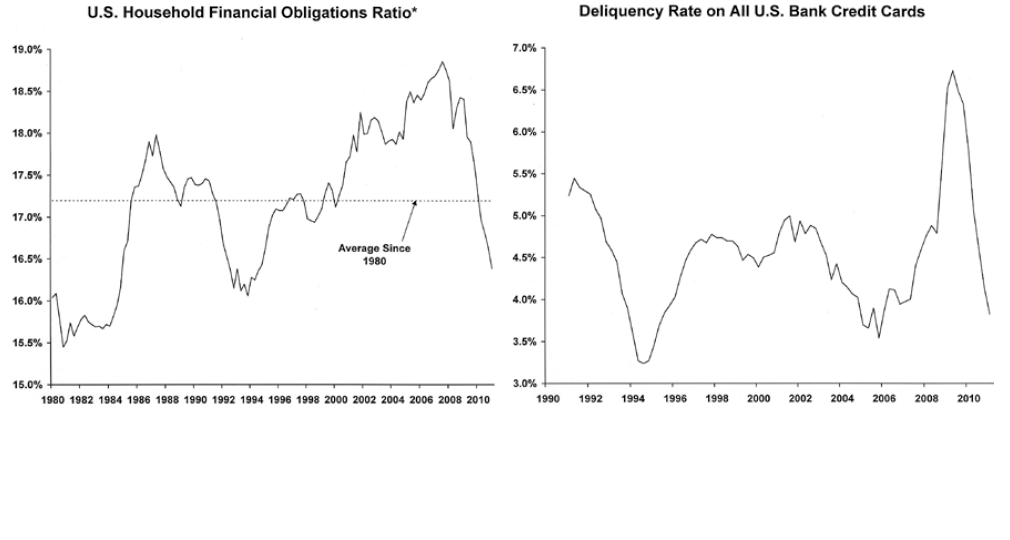

But even more surprising is the recovering health of US consumers. Take a look at the charts below—both show big reductions in the financial stress for the average consumer. The chart on the left shows the percentage of income that goes to interest payments. Lower rates definitely are helping, but debt reduction is also contributing. It’s the chart on the right that surprises the most…

As this chart shows, the delinquency rate on credit cards has collapsed back to 2006 levels. The debt crisis for households may be coming to an end.

As we never tire of saying, we don’t invest in the US economy, we invest in publicly traded corporations. Our investments cannot prosper long term unless the US economy improves, but for now we are focused on high profits and strong balance sheets rather than high unemployment or the debt ceiling.

Since the market bottomed in the middle of June our portfolios have performed well—about doubling the gains for the S&P 500. Here’s hoping that this is an indication of how we do over the remainder of the year.

Best regards,

Daniel A. Ogden

Dock Street Asset Management, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. You should not assume that any discussion or information contained in this letter serves as the receipt of, or as a substitute for, personalized investment advice from Dock Street Asset Management, Inc.

It is published solely for informational purposes and is not to be construed as a solicitation nor does it constitute advice, investment or otherwise.

To the extent that a reader has questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional advisor of their choosing.

A copy of our Form ADV Part II regarding our advisory services and fees is available upon request.

Our comments are an expression of opinion. While we believe our statements to be true, they always depend on the reliability of our own credible sources. Past performance is no guarantee of future returns.

")