The former need to be avoided, while the latter create opportunity

The pain of loss is much more powerful than the pleasure we get from gain. Maybe this widespread trait developed over hundreds of thousands of years worrying about famine while huddled in a cave. Whatever the reason, dealing with the emotions generated by losses is the primary challenge faced by investors.

Investors are mistaken if they think that all losses need to be avoided—this is the promise of market timing gurus. Our view is that temporary losses are nearly unavoidable (and part of the cost of passive investing) but knowing when capital might be destroyed permanently is a key to long-term investment success.

We’ve lived through two bouts of permanent loss in the last 15 years—first, the Dotcom bubble and then the Financial Crisis of 2008. In both cases, many stocks became virtually worthless—remember CMGI in 2003 and AIG in 2008?

In both cases, during the collapse phase, many investors believed the losses to be temporary. We believe the same pattern is playing out today in commodities in general and energy in particular. Billions in capital in those areas face permanent destruction, while the market continues to bet that the worst is over.

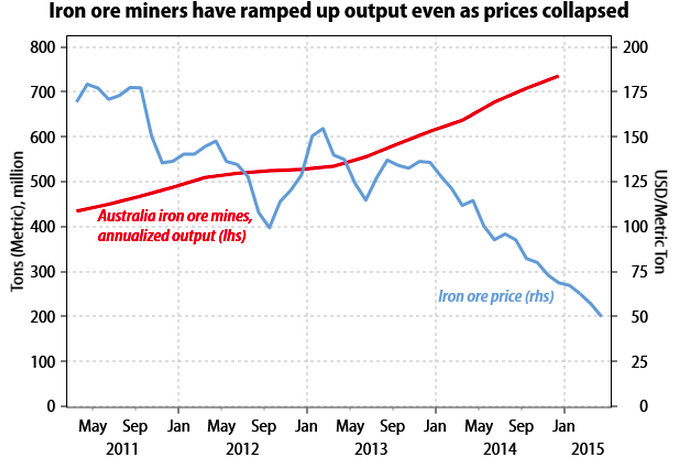

We’ve written a lot about energy, but take a look at this chart of iron ore prices.

This is the same pattern as energy — 1) Massive investment over the last 15 years creates, 2) huge increases in production as, 3) demand from China moderates.

Commodity prices don’t need to go to zero or even much lower to cause bankruptcies throughout the sector. Too many companies (mostly small ones in energy) have borrowed money based on much higher prices than can be obtained today. As someone once said, “The assets are soft, but the debts are rock solid.”

We believe that protection against permanent loss is crucial for investment success and that’s why we plan to avoid the commodity sector.

But what about the temporary losses? Those occur during market corrections, but are also present in major bear markets. Avoiding tech in 2000 and financials in 2008 and just holding on to the unaffected sectors produced enormous gains in subsequent years.

In our next note, we will take a stab at identifying the best candidates that could trigger the next market correction. An event that will produce temporary losses and opportunities for future gains.

Best regards,

Daniel A. Ogden

Disclosure: Dock Street Asset Management, Inc. and our clients may own securities. This article is not intended to be used as investment advice.

Dock Street Asset Management, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. You should not assume that any discussion or information contained in this letter serves as the receipt of, or as a substitute for, personalized investment advice from Dock Street Asset Management, Inc.

It is published solely for informational purposes and is not to be construed as a solicitation nor does it constitute advice, investment or otherwise.

To the extent that a reader has questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional advisor of their choosing.

A copy of our Form ADV Part II regarding our advisory services and fees is available upon request.

Our comments are an expression of opinion. While we believe our statements to be true, they always depend on the reliability of our own credible sources. Past performance is no guarantee of future returns.

")