They often have

Last week Evan McGoff made the reasonable argument that a recession is unlikely when so many economic indicators trend higher, not lower. The bearish (pessimistic) view is that these same indicators will result in higher inflation readings and the Federal Reserve will keep raising rates until there’s a recession.

We don’t think prosperity causes inflation. But there are some at the Federal Reserve who seem to think that. The risk is that the Fed will go too far in raising interest rates and stumble into a recession. They’ve done it before.

If the Fed is focused on the Consumer Price Index (CPI) then the odds of a mistake are higher. The CPI is flawed in many ways, but how it measures housing inflation is the worst. One of the largest factors in calculating housing inflation is a strange concept called “Owners’ Equivalent Rent”. In other words, what rent would a homeowner pay to rent the house they already own?

This goofy CPI measure of housing costs ignores the low interest rates most homeowners are paying right now. It’s estimated that two-thirds of those with a mortgage are at 4% or lower—many below 3%. But the CPI essentially shows the opposite, a rising imaginary cost that homeowners don’t actually pay.

Based on the CPI, the Fed is seeing rising costs of housing, something they want to combat. But in reality, millions of homeowners have locked in more attractive housing costs than the current going rates.

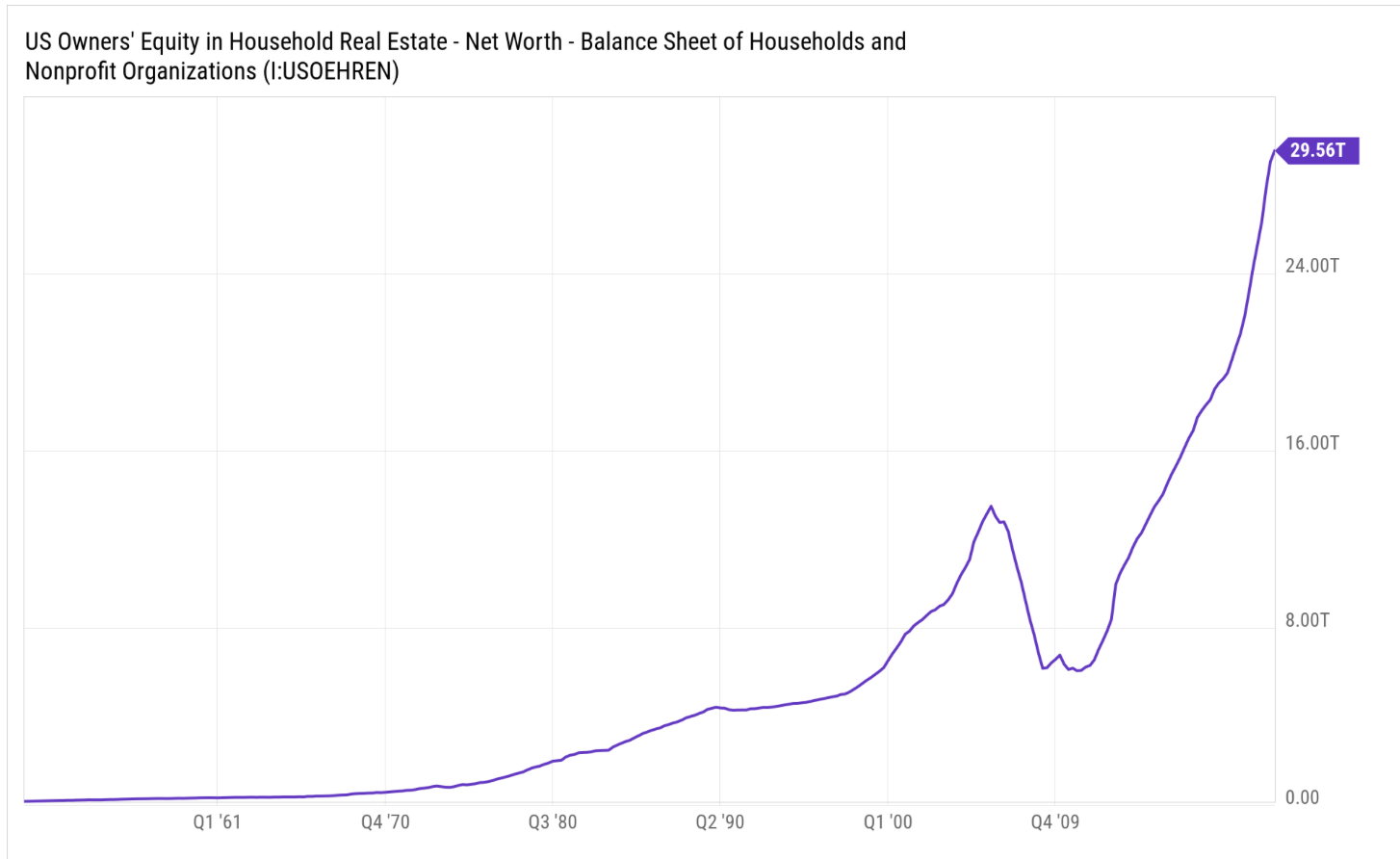

Household Real Estate Equity

The chart above from Ben Carlson illustrates the home equity for all US households—nearly $30 trillion. So most US homeowners are benefiting from low fixed interest rates on their mortgage and have massive cost-free home equity, leaving more money in their pockets. The CPI misses all of this, thereby overstating housing inflation.

If the Federal Reserve puts too much weight on “housing inflation” as measured by the CPI, then a policy accident is more likely. That accident will drive us into a recession and lower stock prices.

While we disagree with this outlook, it remains the primary risk investors face in 2023.

Best regards,

Daniel A. Ogden

Dock Street Asset Management, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. You should not assume that any discussion or information contained in this letter serves as the receipt of, or as a substitute for, personalized investment advice from Dock Street Asset Management, Inc.

It is published solely for informational purposes and is not to be construed as a solicitation nor does it constitute advice, investment or otherwise.

To the extent that a reader has questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional advisor of their choosing.

A copy of our Form ADV Part II regarding our advisory services and fees is available upon request.

Our comments are an expression of opinion. While we believe our statements to be true, they always depend on the reliability of our own credible sources. Past performance is no guarantee of future returns.

")