Two extremes don’t equal balance

The Federal Reserve has been implementing emergency policies for over a decade now. In plain terms, they kept short term interest rates extremely low and made it easy to borrow.

These policies made it easy for banks to pay little-to-no interest on checking and savings accounts. If bonds only pay about 2% interest, then leaving cash in bank accounts yielding nothing isn’t much different. Depositors got used to the meager compensation on their savings, and banks got used to the cheap funding.

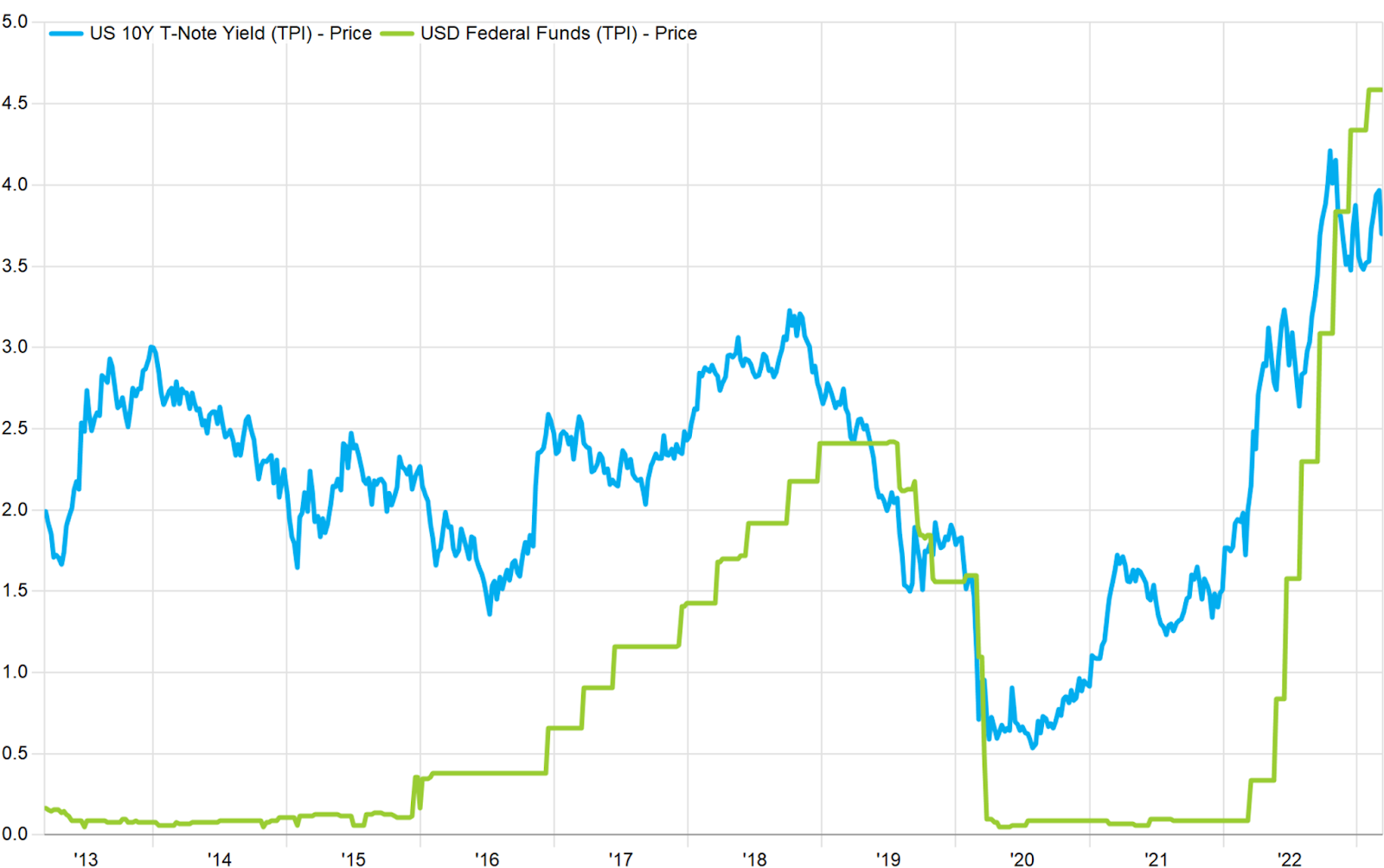

The Fed Funds rate in Green, set by a committee. The 10 Year Treasury bond rate in Blue, set by markets.

Inflation started picking up in 2021, and the Fed was slow to raise interest rates in response. Then in 2022, they moved to the opposite extreme, raising rates from 0% to just over 4%. By raising interest rates so quickly, the Fed woke up depositors from their complacency, but apparently the bankers remained stuck in theirs.

Lately it’s typical to hear people talk about where they’ve moved their short term cash to get a yield. What this does is slowly drain cash deposits from banks that pay so little into the institutions that pay more.

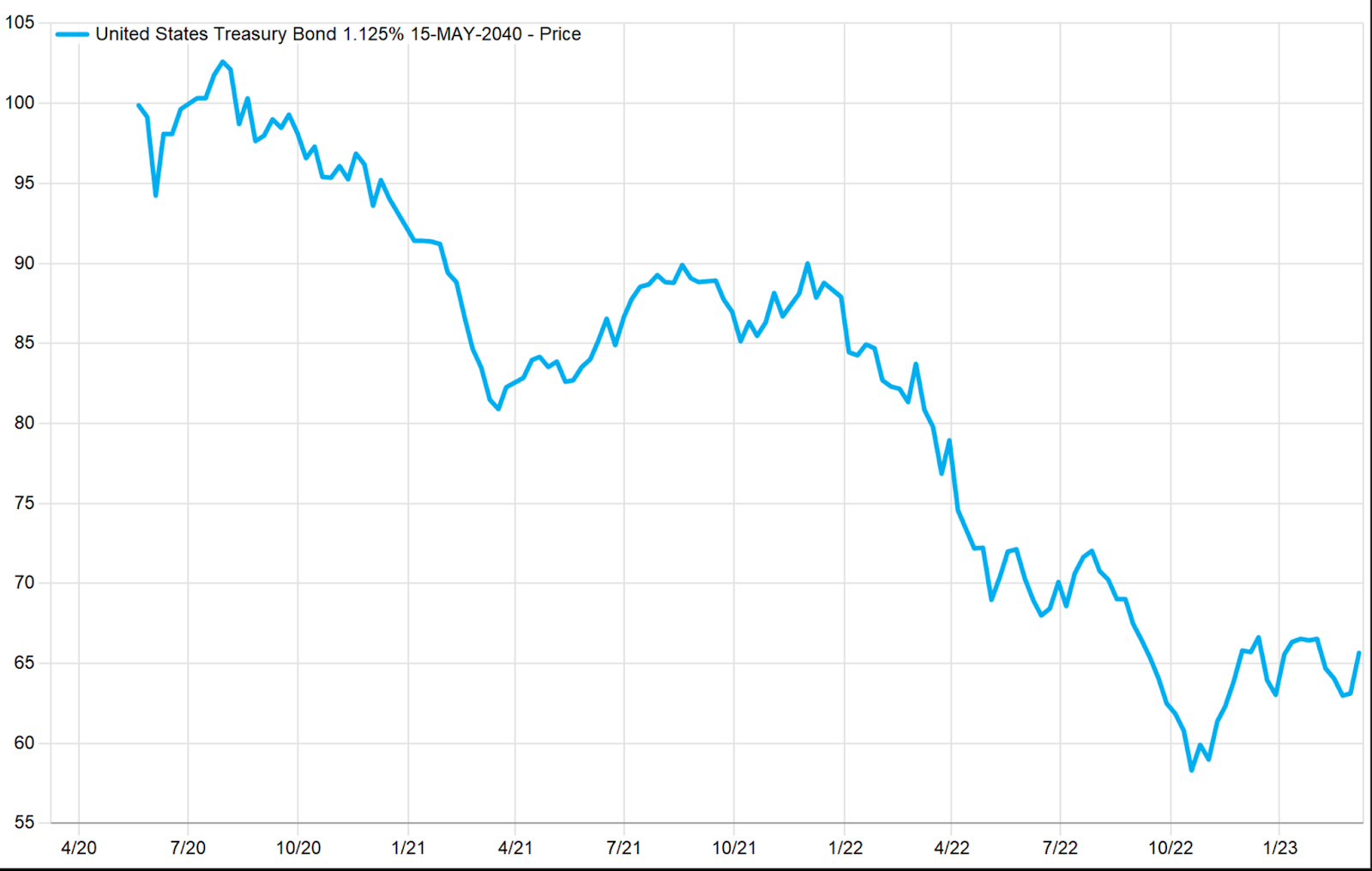

Rising interest rates have had another effect on banks—it decreases the value of many of the longer dated bonds they own. Silicon Valley Bank, and many others like it, have bought longer term bonds over the last few years, hoping to earn higher interest than what was being paid on short term bonds.

Long term bonds are very sensitive to changes in interest rates. As rates rise, the value of long term bonds fall since the price must reflect the new market rate of interest. The chart below reveals what happened to the value of a 20-year bond purchased in May 2020. It has fallen 35%!

Banks all around the world own assets that look like this. Selling them now means taking major losses.

The combination of these two trends—deposits leaving and the investments falling in value—create a vulnerable position for banks. For many of them, the value of what they own is less than what they owe. And if customers all come demanding their deposits at once, you have a classic bank run.

It takes two to tango, so to speak. Banks should have known better. But so should the Fed.

The risk controls at Silicon Valley Bank were clearly insufficient, and that’s probably true of banks elsewhere. And yet, the Federal Reserve’s extreme policy playbook for the last decade plus was all for the goal of preventing the banking system from collapsing. The Fed’s more recent singular focus on inflation meant ignoring a solvency crisis they’ve perpetuated.

Banks now look especially unappealing, even if a crisis is averted. They’ll have to pay depositors higher interest to keep them, and the value of what they’ve bought won’t necessarily recover anytime soon. The Fed needs to change tack, and take its focus away from inflation (which is gradually improving) and get back to its core mission: being the lender of last resort to the banking system. We’re happy to have sold the banks in 2007, and haven’t looked back.

Best regards,

Evan McGoff

Dock Street Asset Management, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. You should not assume that any discussion or information contained in this letter serves as the receipt of, or as a substitute for, personalized investment advice from Dock Street Asset Management, Inc.

It is published solely for informational purposes and is not to be construed as a solicitation nor does it constitute advice, investment or otherwise.

To the extent that a reader has questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional advisor of their choosing.

A copy of our Form ADV Part II regarding our advisory services and fees is available upon request.

Our comments are an expression of opinion. While we believe our statements to be true, they always depend on the reliability of our own credible sources. Past performance is no guarantee of future returns.